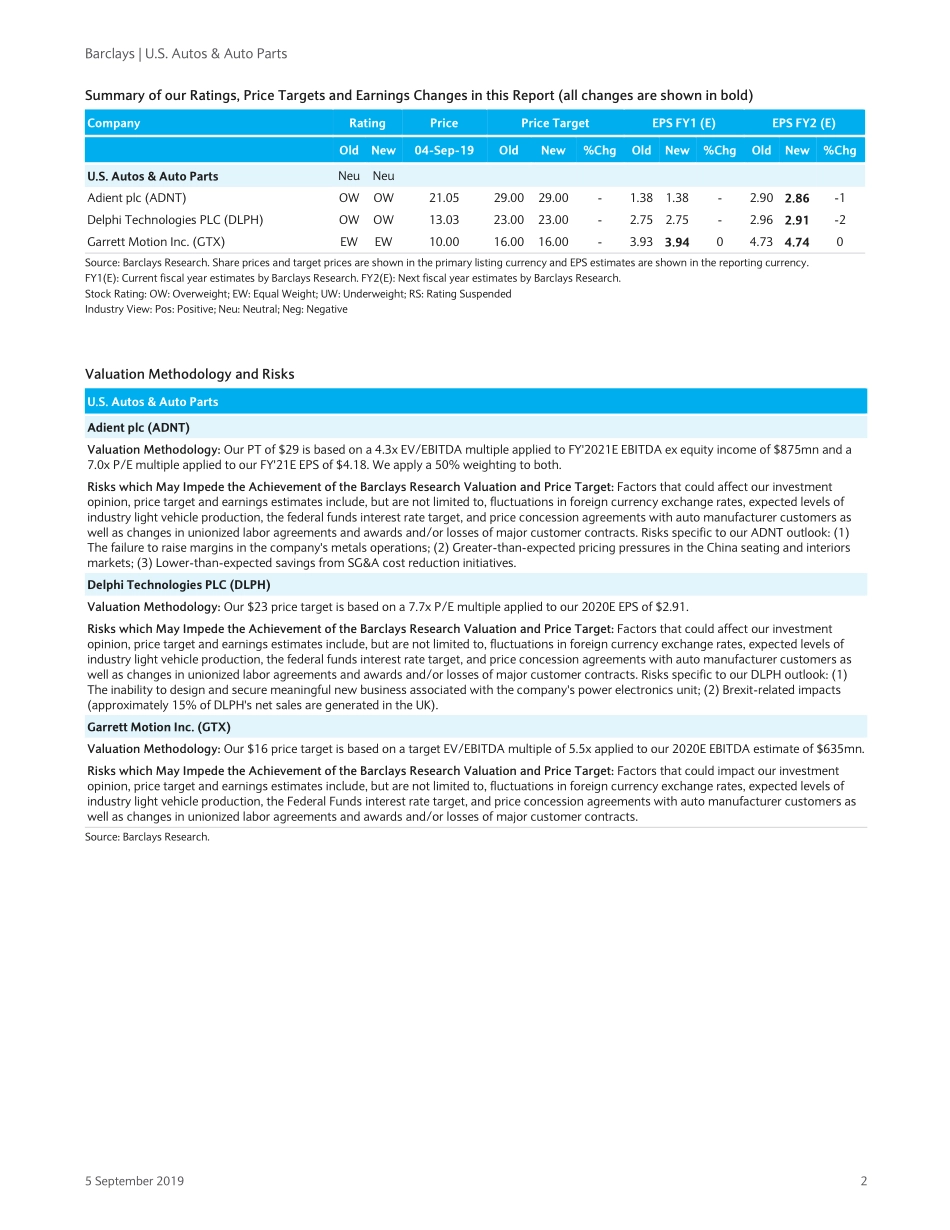

EquityResearch5September2019FOCUSBarclaysCapitalInc.and/oroneofitsaffiliatesdoesandseekstodobusinesswithcompaniescoveredinitsresearchreports.Asaresult,investorsshouldbeawarethatthefirmmayhaveaconflictofinterestthatcouldaffecttheobjectivityofthisreport.Investorsshouldconsiderthisreportasonlyasinglefactorinmakingtheirinvestmentdecision.PLEASESEEANALYSTCERTIFICATION(S)ANDIMPORTANTDISCLOSURESBEGINNINGONPAGE25.Restricted-ExternalU.S.Autos&AutoPartsLatecycleautopartLBOsarepossibleLBOscouldprovideafloortovaluations.Investorshavebeguntotakenoteaftertheannouncementoftwodealsthisyear(MagnettiMarelliandTower)seemstobeliecommonwisdomthatit’stoolateinthecyclefor‘takeprivate’transactions.UsingabackoftheenvelopeLBOframework,weseethegreatestpotentialinAXL.Latecycleautopartsdealhistoryislessbadtheninvestorsthink.Autopartsdon’tmeetmanyofthecommoncriteriaforLBOsandpublicinvestors(andwethinkPEsponsors)pointtolatecycledealsfromthemid-2000sasproofthatautopartsLBOswon’twork.Buttwotheofdeals(DanaandTower)appeartohaveeventuallyattractiveIRRseveninthefaceoftheGreatRecession,andanothersetoftransactions(therollupofmetalformingintoHHIandMetaldyne)washighlysuccessful.Somekeysuccessfactorsthatemergeincludea)buycheap(ofcourse),b)thinkaboutplatformstobuyevencheaperlater,andc)havefollow-onfundsavailableforbolt-on/debtbuyback.First-cutscreenforcompaniestoevaluatefurther.Usingascreenofa)equitymarketcap<$3bnandb)stockpriceunder50%ofoneyearhigh,yields4companiestoexamineinmoredepth:AXL,DLPH,GTXandADNT.AXLcashflowsmakeitthemostpromisingcandidate.WeexamineAXL,DLPH,ADNTandGTXforpotentialreturns–bothinabasecaseasis,basecasewithassetsales,andadownsiderecession/recoveryscenario.ToexaminetheLBO,wecreated‘backoftheenvelope’LBOmodelsforeachsupplier.•AXLmaybethebestall-aroundcandidateforatake–privatetransaction,largelyduetoitsstrongcashflowgeneration(whichisstillstrongdespiterecentmissteps).ReturnscouldbeenhancedfurtherbysellingpartsoftheMetaldynebusinessitacquired,evenifforlessthanwhatwasoriginallypa...