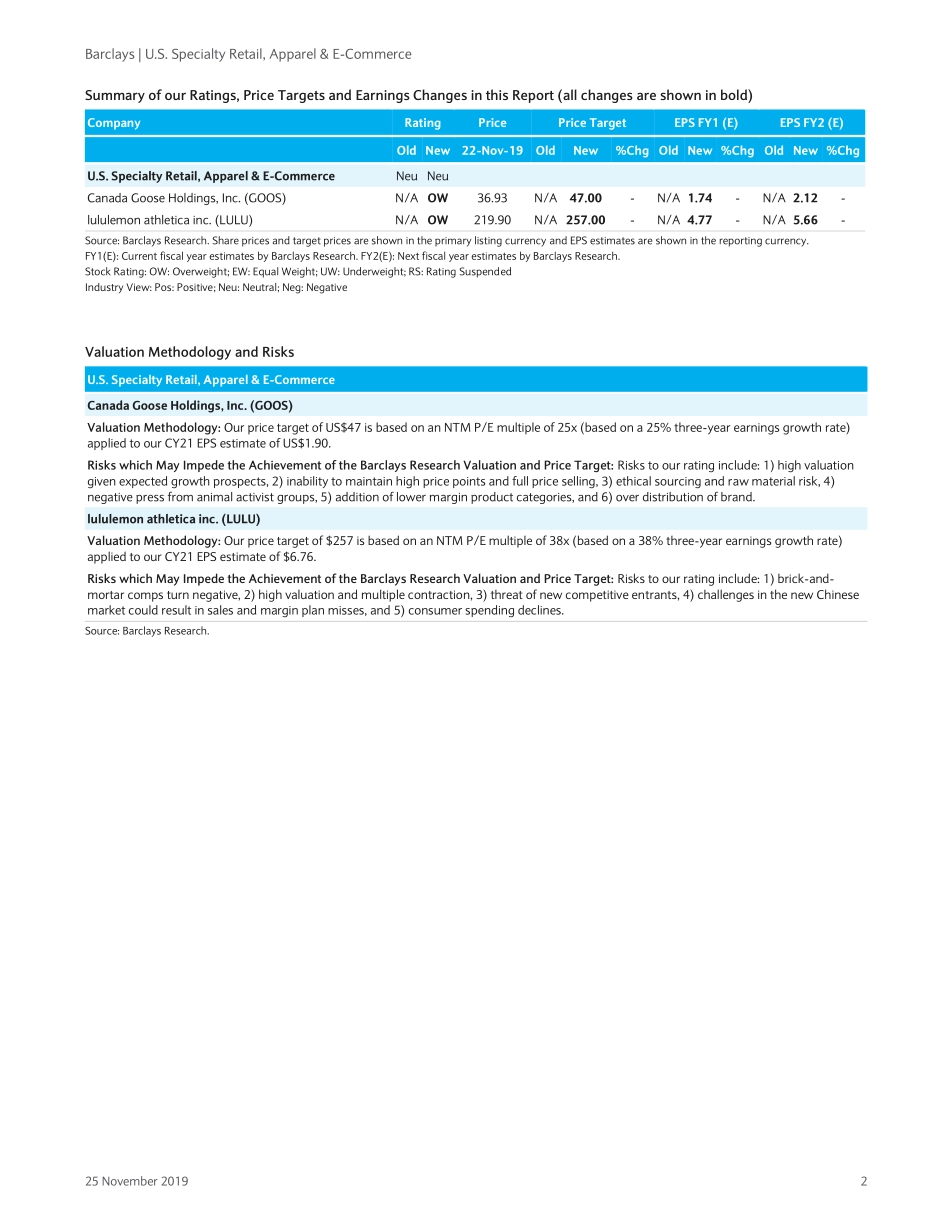

EquityResearch25November2019COREBarclaysCapitalInc.and/oroneofitsaffiliatesdoesandseekstodobusinesswithcompaniescoveredinitsresearchreports.Asaresult,investorsshouldbeawarethatthefirmmayhaveaconflictofinterestthatcouldaffecttheobjectivityofthisreport.Investorsshouldconsiderthisreportasonlyasinglefactorinmakingtheirinvestmentdecision.PLEASESEEANALYSTCERTIFICATION(S)ANDIMPORTANTDISCLOSURESBEGINNINGONPAGE27.Restricted-InternalU.S.SpecialtyRetail,Apparel&E-CommerceInitiatingCoverage:GOOS,LULUInitiatingGOOSandLULUatOverweight.WeareaddingtoourcoverageuniversewithtwoCanadiangloballuxurybrands,GOOSandLULU.Weusethesameinvestmentframeworkandmethodology,bothqualitativeandquantitative,asweoutlinedinourrecentinitiationreport,InitiatingCoverage:IntroducingPRISM360º,aHolisticApproachtoRetail(Nov12,2019).Wenoteseveralsimilarities,notwithstandingvaluation,ofthesetwoglobalgrowthbrands,whichwehighlightbelow.Brandswithpricingpower.TheGOOSandLULUbrandsarebothrootedinauthenticity,superiorfunctionality,andhighquality,withanelevatedcustomerexperience–bothinstoreandonline.GOOSisintheveryearlystagesofgrowthrelativetoLULU.WithtrailingtwelvemonthsalesofaboutUS$700mn,webelieveGOOShassignificantmarketshareopportunity.WelooktothepaththatLULUhastakenasaroadmapforboththegrowthpotentialandthechallengesthatcomewiththerapidexpansionofahighlydesirablebrand.Bothcompanieshavevertically-integratedretail,withtheopportunitytocapturefullmarginpotentialastheycansellproduct,andinmanycasesoftenselloutofproduct,atfullprice.GOOSalsogeneratesroughlyhalfitsbusinessthroughwholesalebutisshiftingitsmodeltowardshigher-margindirect-to-consumerretail.Globalgrowthopportunity.LULUgeneratesthevastmajorityofitssalesfromtheNorthAmericanmarket,withthemostsignificantgrowthopportunityfromquadruplingitsbusinessintheChinamarket.GOOSgenerates35%ofsalesfromCanada,30%fromtheU.S.,and34%outsideofNorthAmerica.Bothhavelongrunwaysofglobalgrowthaheadofthem,inourview.Twoendsofthevaluationspectrum.WhileLULUistradingathistoricallyhighval...