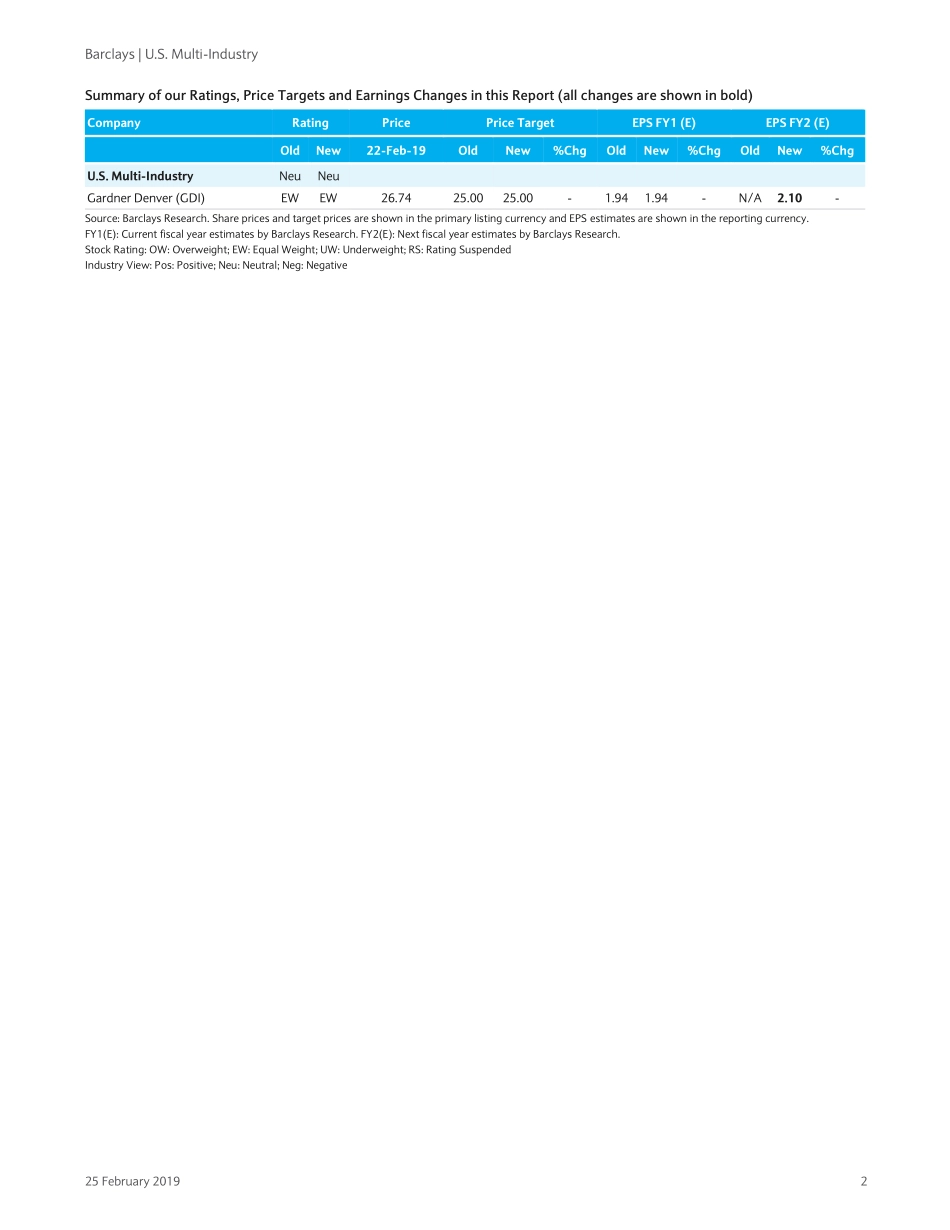

EquityResearch25February2019COREBarclaysCapitalInc.and/oroneofitsaffiliatesdoesandseekstodobusinesswithcompaniescoveredinitsresearchreports.Asaresult,investorsshouldbeawarethatthefirmmayhaveaconflictofinterestthatcouldaffecttheobjectivityofthisreport.Investorsshouldconsiderthisreportasonlyasinglefactorinmakingtheirinvestmentdecision.PLEASESEEANALYSTCERTIFICATION(S)ANDIMPORTANTDISCLOSURESBEGINNINGONPAGE44.Restricted-InternalU.S.Multi-IndustryISCConferenceTakeaways22Multi-IndustrycompaniesattendedourIndustrialsSelectConferenceinMiamionFeb20-21.Overall,ourimpressionontop-linedemandwasthatmostareasofweaknessinQ4havenotimprovedyetinQ1,butthissoftnessdoesnotseemtohavespreadtoothermarkets.Wedidhearfurtherremindersthat2019issomethingofaback-endloadedyear,withEPSgrowthmoreweightedinthe2Hformanycompanies.Giventheorganictop-lineslowdownthisyear,ongoingcheapdebt/lowfinancingcosts,aswellasthecommentaryfromvariouscorporates,wecameawayfromtheconferencethinkingthattheconditionsareinplaceforheightenedMulti-IndustryM&Aactivity.Intermsofprofitability,price/costheadwindsarelingeringforseveralcompanies,butmostseemconfidentthattheseshouldlargelydissipatebyQ2(assumingstatusquointhetariffenvironment);weestimatethatoverallsectorincrementalmarginsrecoverto~30%in2019,after~15%in2018.Investorsentiment:TheAudienceResponseSurveydatasuggeststhat,followingtherun-upinthesectorthisyear(+18%againsttheS&P+11%),investorsarenotwillingtore-ratevaluationmultiplesmuchhigher;onaverage,theARSdatashowedthatinvestorsarewillingtopay16.0xintermsof2019P/EforMulti-Industrynames,against~17.2xayearago.RelativetoitsLTaverage,theMIsectorisataslightP/Epremium(~0.5standarddeviationsaboveitshistoricalrelativemultiple).Hence,althoughthestockslikelyperformwellasweawaitChina-UStradetensionresolutions,thepathforfurtheroutperformancefollowingsuchnewsislessclear.All-in,sincetheconferenceayearago,Industrialstocksaredownslightly,againsttheS&Pupslightly;weremaincomfortablewithourNeutralIndustryweighting.Withinthesector,weconti...