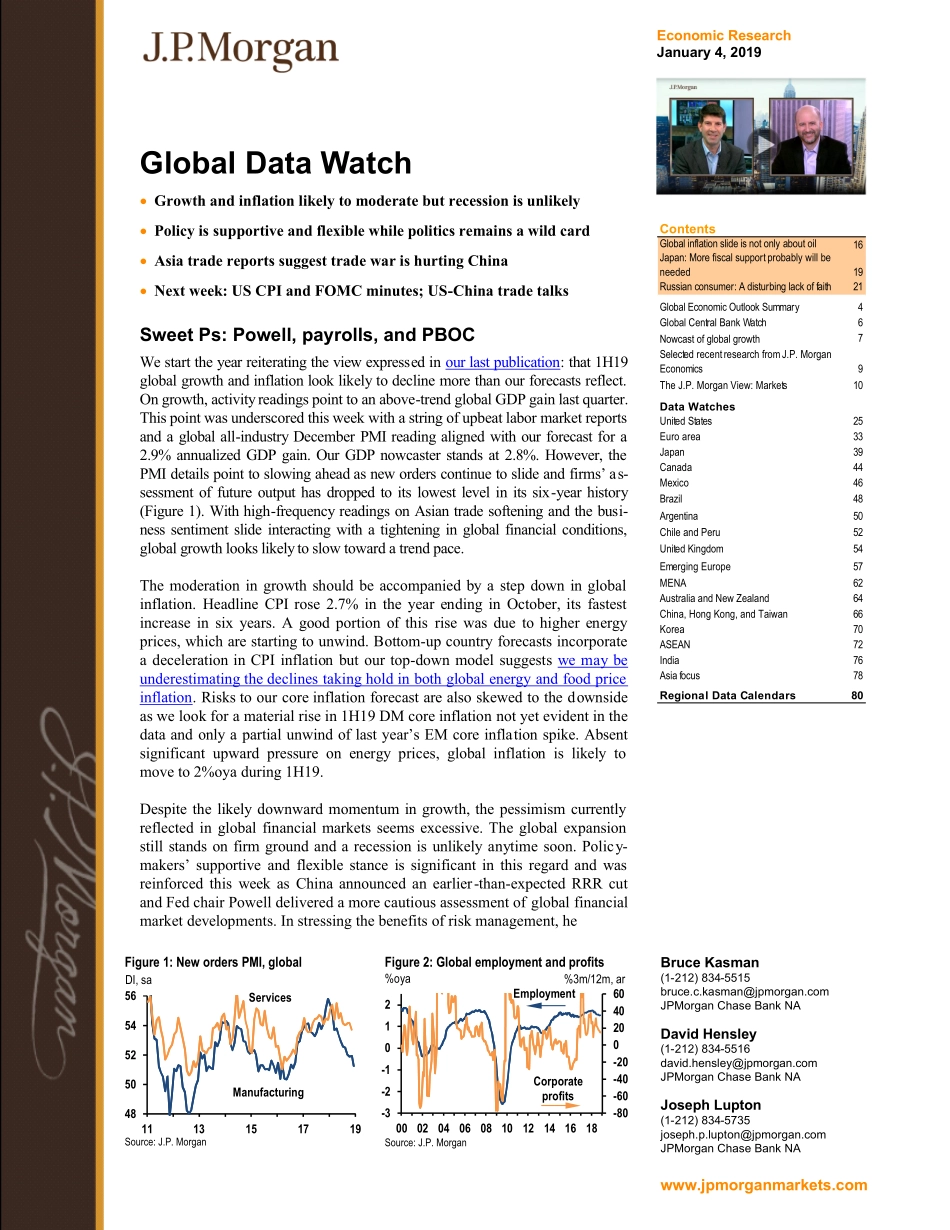

EconomicResearchJanuary4,2019GlobalDataWatchGrowthandinflationlikelytomoderatebutrecessionisunlikelyPolicyissupportiveandflexiblewhilepoliticsremainsawildcardAsiatradereportssuggesttradewarishurtingChinaNextweek:USCPIandFOMCminutes;US-ChinatradetalksSweetPs:Powell,payrolls,andPBOCWestarttheyearreiteratingtheviewexpressedinourlastpublication:that1H19globalgrowthandinflationlooklikelytodeclinemorethanourforecastsreflect.Ongrowth,activityreadingspointtoanabove-trendglobalGDPgainlastquarter.Thispointwasunderscoredthisweekwithastringofupbeatlabormarketreportsandaglobalall-industryDecemberPMIreadingalignedwithourforecastfora2.9%annualizedGDPgain.OurGDPnowcasterstandsat2.8%.However,thePMIdetailspointtoslowingaheadasneworderscontinuetoslideandfirms’as-sessmentoffutureoutputhasdroppedtoitslowestlevelinitssix-yearhistory(Figure1).Withhigh-frequencyreadingsonAsiantradesofteningandthebusi-nesssentimentslideinteractingwithatighteninginglobalfinancialconditions,globalgrowthlookslikelytoslowtowardatrendpace.Themoderationingrowthshouldbeaccompaniedbyastepdowninglobalinflation.HeadlineCPIrose2.7%intheyearendinginOctober,itsfastestincreaseinsixyears.Agoodportionofthisrisewasduetohigherenergyprices,whicharestartingtounwind.Bottom-upcountryforecastsincorporateadecelerationinCPIinflationbutourtop-downmodelsuggestswemaybeunderestimatingthedeclinestakingholdinbothglobalenergyandfoodpriceinflation.Riskstoourcoreinflationforecastarealsoskewedtothedownsideaswelookforamaterialrisein1H19DMcoreinflationnotyetevidentinthedataandonlyapartialunwindoflastyear’sEMcoreinflationspike.Absentsignificantupwardpressureonenergyprices,globalinflationislikelytomoveto2%oyaduring1H19.Despitethelikelydownwardmomentumingrowth,thepessimismcurrentlyreflectedinglobalfinancialmarketsseemsexcessive.Theglobalexpansionstillstandsonfirmgroundandarecessionisunlikelyanytimesoon.Policy-makers’supportiveandflexiblestanceissignificantinthisregardandwasreinforcedthisweekasChinaannouncedanearlier-than-expectedRRR...