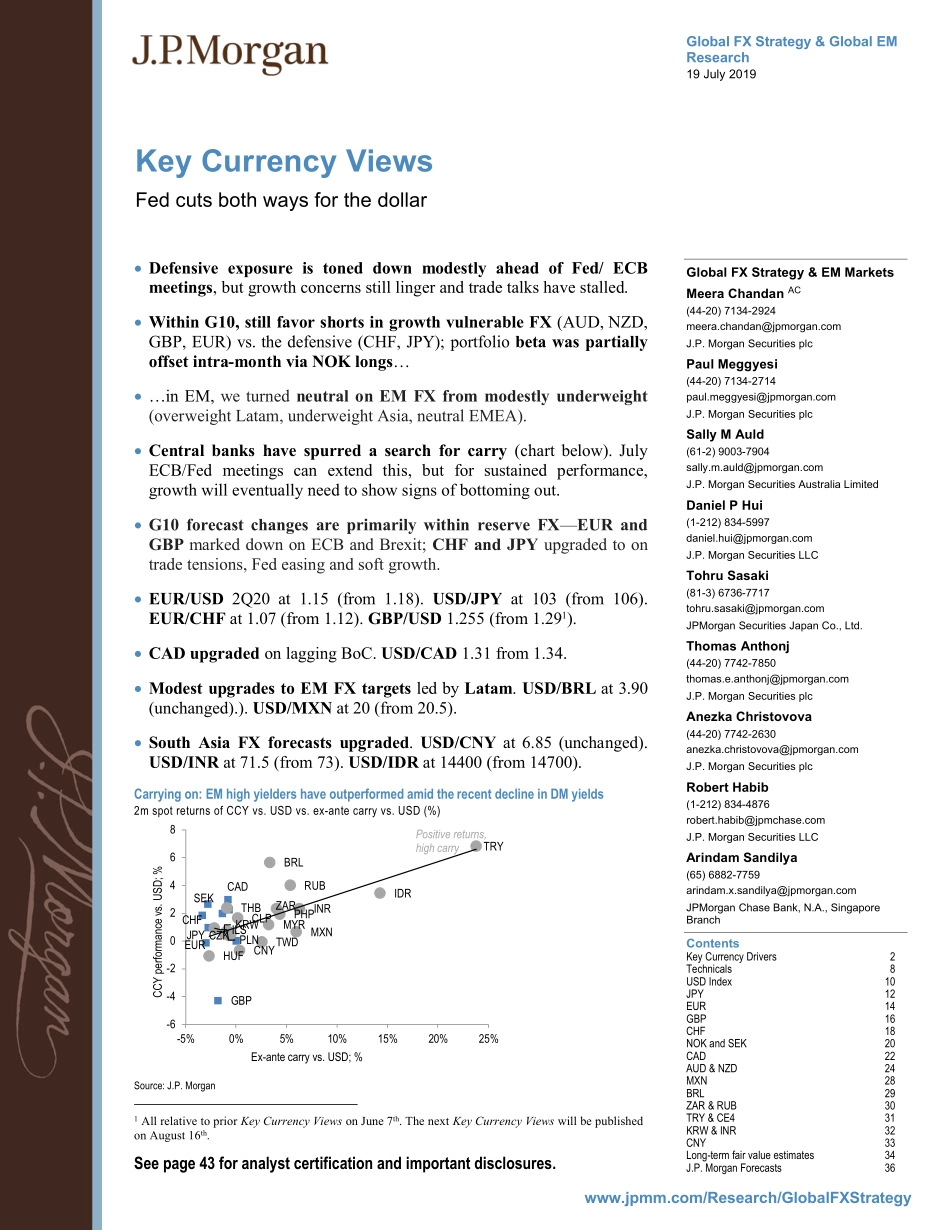

www.jpmm.com/Research/GlobalFXStrategyGlobalFXStrategy&GlobalEMResearch19July2019KeyCurrencyViewsFedcutsbothwaysforthedollarGlobalFXStrategy&EMMarketsMeeraChandanAC(44-20)7134-2924meera.chandan@jpmorgan.comJ.P.MorganSecuritiesplcPaulMeggyesi(44-20)7134-2714paul.meggyesi@jpmorgan.comJ.P.MorganSecuritiesplcSallyMAuld(61-2)9003-7904sally.m.auld@jpmorgan.comJ.P.MorganSecuritiesAustraliaLimitedDanielPHui(1-212)834-5997daniel.hui@jpmorgan.comJ.P.MorganSecuritiesLLCTohruSasaki(81-3)6736-7717tohru.sasaki@jpmorgan.comJPMorganSecuritiesJapanCo.,Ltd.ThomasAnthonj(44-20)7742-7850thomas.e.anthonj@jpmorgan.comJ.P.MorganSecuritiesplcAnezkaChristovova(44-20)7742-2630anezka.christovova@jpmorgan.comJ.P.MorganSecuritiesplcRobertHabib(1-212)834-4876robert.habib@jpmchase.comJ.P.MorganSecuritiesLLCArindamSandilya(65)6882-7759arindam.x.sandilya@jpmorgan.comJPMorganChaseBank,N.A.,SingaporeBranchSeepage43foranalystcertificationandimportantdisclosures.DefensiveexposureistoneddownmodestlyaheadofFed/ECBmeetings,butgrowthconcernsstilllingerandtradetalkshavestalled.WithinG10,stillfavorshortsingrowthvulnerableFX(AUD,NZD,GBP,EUR)vs.thedefensive(CHF,JPY);portfoliobetawaspartiallyoffsetintra-monthviaNOKlongs……inEM,weturnedneutralonEMFXfrommodestlyunderweight(overweightLatam,underweightAsia,neutralEMEA).Centralbankshavespurredasearchforcarry(chartbelow).JulyECB/Fedmeetingscanextendthis,butforsustainedperformance,growthwilleventuallyneedtoshowsignsofbottomingout.G10forecastchangesareprimarilywithinreserveFX—EURandGBPmarkeddownonECBandBrexit;CHFandJPYupgradedtoontradetensions,Fedeasingandsoftgrowth.EUR/USD2Q20at1.15(from1.18).USD/JPYat103(from106).EUR/CHFat1.07(from1.12).GBP/USD1.255(from1.291).CADupgradedonlaggingBoC.USD/CAD1.31from1.34.ModestupgradestoEMFXtargetsledbyLatam.USD/BRLat3.90(unchanged).).USD/MXNat20(from20.5).SouthAsiaFXforecastsupgraded.USD/CNYat6.85(unchanged).USD/INRat71.5(from73).USD/IDRat14400(from14700).Carryingon:EMhighyieldershaveoutperformedamidtherecentde...