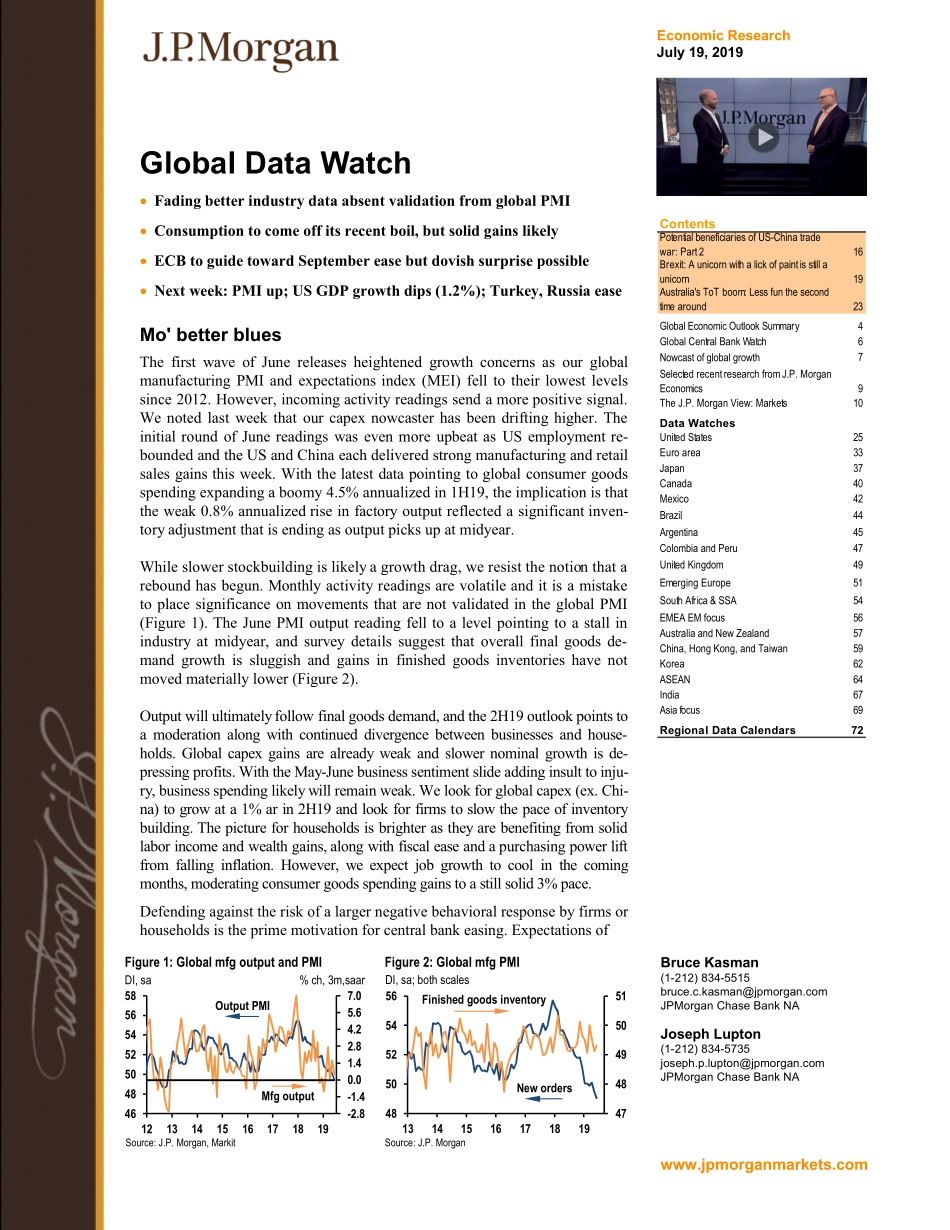

EconomicResearchJuly19,2019GlobalDataWatchFadingbetterindustrydataabsentvalidationfromglobalPMIConsumptiontocomeoffitsrecentboil,butsolidgainslikelyECBtoguidetowardSeptembereasebutdovishsurprisepossibleNextweek:PMIup;USGDPgrowthdips(1.2%);Turkey,RussiaeaseMo'betterbluesThefirstwaveofJunereleasesheightenedgrowthconcernsasourglobalmanufacturingPMIandexpectationsindex(MEI)felltotheirlowestlevelssince2012.However,incomingactivityreadingssendamorepositivesignal.Wenotedlastweekthatourcapexnowcasterhasbeendriftinghigher.TheinitialroundofJunereadingswasevenmoreupbeatasUSemploymentre-boundedandtheUSandChinaeachdeliveredstrongmanufacturingandretailsalesgainsthisweek.Withthelatestdatapointingtoglobalconsumergoodsspendingexpandingaboomy4.5%annualizedin1H19,theimplicationisthattheweak0.8%annualizedriseinfactoryoutputreflectedasignificantinven-toryadjustmentthatisendingasoutputpicksupatmidyear.Whileslowerstockbuildingislikelyagrowthdrag,weresistthenotionthatareboundhasbegun.MonthlyactivityreadingsarevolatileanditisamistaketoplacesignificanceonmovementsthatarenotvalidatedintheglobalPMI(Figure1).TheJunePMIoutputreadingfelltoalevelpointingtoastallinindustryatmidyear,andsurveydetailssuggestthatoverallfinalgoodsde-mandgrowthissluggishandgainsinfinishedgoodsinventorieshavenotmovedmateriallylower(Figure2).Outputwillultimatelyfollowfinalgoodsdemand,andthe2H19outlookpointstoamoderationalongwithcontinueddivergencebetweenbusinessesandhouse-holds.Globalcapexgainsarealreadyweakandslowernominalgrowthisde-pressingprofits.WiththeMay-Junebusinesssentimentslideaddinginsulttoinju-ry,businessspendinglikelywillremainweak.Welookforglobalcapex(ex.Chi-na)togrowata1%arin2H19andlookforfirmstoslowthepaceofinventorybuilding.Thepictureforhouseholdsisbrighterastheyarebenefitingfromsolidlaborincomeandwealthgains,alongwithfiscaleaseandapurchasingpowerliftfromfallinginflation.However,weexpectjobgrowthtocoolinthecomingmonths,moderatingconsumergoodsspendinggainstoastillsolid3%pace.Defendingagainsttheris...